Why M&A Transactions Are Complex Business Changes

An M&A transaction is one of the most consequential moves a company can make. It changes ownership, strategy, finances, and culture—often all at once—so every step must be handled with care.

Why the process is demanding:

- Strategy Development – Set measurable goals and clear target criteria.

- Due Diligence – Verify financials, uncover liabilities, and confirm fit.

- Valuation & Negotiation – Agree on a fair price and balanced terms.

- Deal Structuring – Choose between stock, asset, or merger form.

- Regulatory Approval – Satisfy antitrust and securities rules.

- Integration Planning – Capture synergies once the deal closes.

Even a mid-sized deal can take 6–18 months and generate thousands of pages of disclosure. Managed well, it open ups growth; mismanaged, it can erase value just as quickly.

I’m David Fritch, and over four decades in law and business I’ve guided owners, executives, and investors through acquisitions, divestitures, and restructurings. The insights below are drawn from those experiences and aim to help you approach your own M&A transaction with confidence.

M&a transaction terms made easy:

Understanding the Fundamentals: Mergers vs. Acquisitions

When you’re considering an M&A transaction, it’s crucial to understand what you’re actually getting into. While people often use “merger” and “acquisition” as if they mean the same thing, they’re actually quite different beasts with their own legal and financial quirks.

Think of it this way: if business combinations were dance moves, mergers would be the tango (two partners moving as one), while acquisitions would be more like one dancer lifting the other.

What are Mergers and Acquisitions?

Let’s start with the basics. M&A stands for “mergers and acquisitions” – transactions where companies join forces in various ways. But here’s where it gets interesting.

A merger is like two rivers flowing together to create one bigger river. Two companies decide to combine and create a completely new legal entity. Both original companies disappear, and their shareholders get stock in the shiny new combined company. It’s a true partnership where both companies cease to exist as separate entities.

An acquisition is different. Picture a large river absorbing a smaller stream. One company (usually the bigger one) buys another company and becomes the new owner. The acquiring company keeps going strong, while the target company might continue as a subsidiary or get dissolved entirely.

But wait, there’s more! The M&A world has other flavors too:

Consolidation works similarly to a merger but typically involves multiple companies combining forces. Tender offers happen when a company makes direct offers to shareholders to buy their stock. Then you have the dramatic stuff – hostile takeovers where acquisitions happen without the target company’s board approval, and friendly takeovers where everyone plays nice and cooperates.

| Aspect | Merger | Acquisition |

|---|---|---|

| Legal Structure | Two companies become one new entity | One company absorbs another |

| Company Names | New combined name or one name survives | Acquiring company name typically survives |

| Size of Companies | Usually similar-sized companies | Typically larger company buys smaller |

| Outcome | Shareholders of both companies own the new entity | Target company shareholders receive payment or stock |

Why does this matter? Because these distinctions affect everything from your tax bill to regulatory requirements to how the whole deal gets structured and financed.

Strategic Motivations and Common Types

Companies don’t wake up one morning and decide to pursue an M&A transaction for fun. There are usually compelling strategic reasons behind these complex deals. The main goal? Improved financial performance or reduced risk through various benefits that come from combining forces.

Here’s what typically drives these decisions: Economy of scale helps reduce per-unit costs through increased production volume. Economy of scope lets companies leverage shared resources across different product lines. Market share growth eliminates competition and builds market dominance, while cross-selling opportunities allow companies to offer complementary products to existing customers.

Synergy realization combines operations for greater efficiency. Diversification spreads risk across different markets or industries. Vertical integration gives companies more control over their supply chain. And acquiring new technology provides access to innovative capabilities or intellectual property that might take years to develop internally.

M&A transactions typically fall into three strategic categories. Horizontal acquisitions bring together companies at the same level of the value chain – imagine two competing restaurants merging to increase market share and reduce competition. Vertical acquisitions happen when companies at different stages of the production process combine, like a car manufacturer acquiring a parts supplier to control costs and ensure quality. Conglomerate acquisitions unite companies in completely unrelated industries, often for diversification purposes – such as a technology company acquiring a food service business.

The bottom line? The strategic rationale needs to justify the significant time, cost, and risk involved in any M&A transaction. Without a solid “why,” even the most well-executed deal can become an expensive mistake.

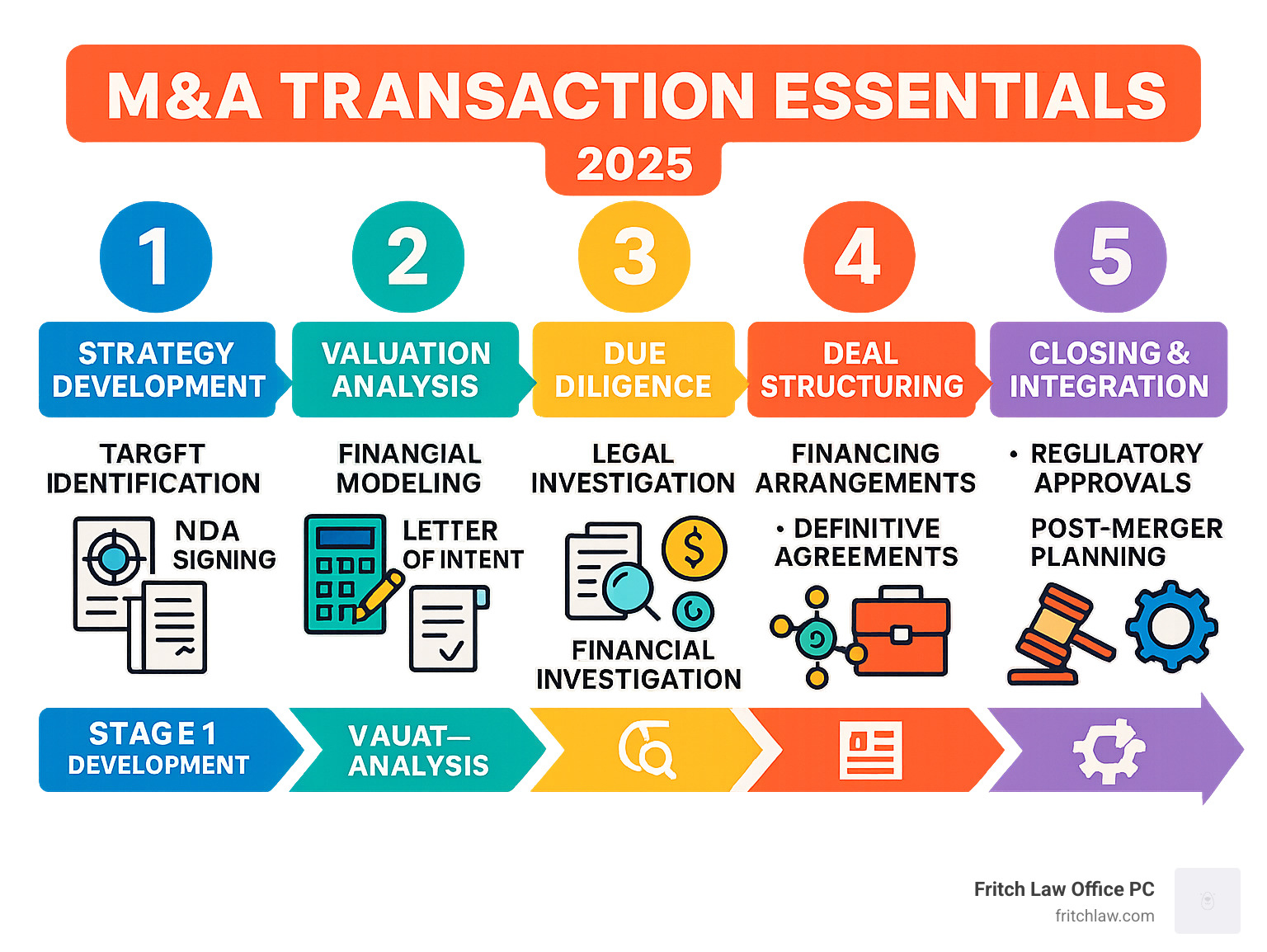

The Anatomy of an M&A Transaction: A Step-by-Step Guide

Think of an M&A transaction as building a house: you need clear plans, solid materials, and the right experts. Most deals follow five broad phases and can last from six months to several years, depending on their complexity.

Stage 1: Strategy Development & Target Identification

Start with why. Define the goal—enter a new market, obtain technology, remove competition—and translate it into measurable criteria (industry, size, geography, finances). Screen companies, open quiet conversations, and protect information with a Non-Disclosure Agreement (NDA). Our methods for developing a rigorous pre-deal M&A strategy offer a practical checklist.

Stage 2: Valuation, Negotiation, and Letter of Intent (LOI)

Tools such as the Price-to-Earnings (P/E) Ratio or Discounted Cash Flow (DCF) translate strategy into numbers. A concise Term Sheet or LOI records price, structure, and exclusivity so both sides can proceed to deeper diligence.

Stage 3: The Critical Role of Due Diligence

Due diligence is a full diagnostic exam—financial, legal, operational, and capitalization. Expect 30-90 days and a request list that easily spans ten pages. Findings often refine price, shift risk allocation, or—when serious—halt the deal. Our Corporate and Commercial Law services streamline this demanding phase.

Stage 4: Deal Structuring, Financing, and Definitive Agreements

A stock sale transfers all assets and liabilities; an asset sale lets the buyer select what to buy; a merger blends entities under state statutes. Cash, equity, seller notes, or third-party debt can fund the purchase. The Purchase and Sale Agreement (PSA) turns business points into binding obligations and protective covenants. Our tax planning attorneys tailor structures for efficiency and risk management.

Stage 5: Closing and Post-Merger Integration

Closing satisfies regulatory, financing, and shareholder conditions; integration turns two organizations into one. Successful plans coordinate systems, people, and culture from day one. Our corporate dissolution counsel keeps the legal house in order while leadership focuses on execution.

Navigating the Legal and Financial Landscape

Beyond procedure, an M&A transaction reshapes capital structure, shareholder rights, and regulatory status. Anticipating these effects early prevents costly surprises.

Financial and Shareholder Implications

Buying a company changes more than the purchase price. Studies show target shareholders generally receive a premium, while acquirer shares can dip until promised synergies appear. Stock-financed deals dilute existing owners and may alter voting control. Cash flow may shift from dividends to debt service or integration costs. Our asset protection lawyer team helps clients weigh these trade-offs.

Key Regulatory and Legal Considerations

Transactions must comply with:

- Antitrust / Competition law – U.S. regulators apply the Clayton Act and the Hart-Scott-Rodino Act; similar rules exist worldwide (see Competition law). Most mid-market deals clear quickly, but those that combine major market share invite extended review.

- Securities law – Public companies face disclosure, proxy, and insider-trading requirements.

- State corporate law – Board duties, shareholder votes, and appraisal rights vary by jurisdiction; our Indiana corporate law guidance ensures compliance.

- Deal-protection measures – No-shop clauses, match rights, and break fees (typically 2–5 % of equity value) secure a friendly agreement without blocking superior offers.

Early alignment with counsel keeps the timeline on track and protects hard-won momentum.

Special Considerations for M&A in Canada

While many principles are universal, cross-border transactions require specific knowledge of local laws. M&A in Canada, for example, has a unique regulatory framework that differs significantly from U.S. practice. Understanding these differences is crucial for any business considering acquisitions north of the border.

The Canadian Regulatory Framework

Canada’s approach to regulating M&A transactions involves multiple layers of oversight, each with its own requirements and timelines. Unlike the more centralized U.S. system, Canadian regulation involves federal and provincial authorities working together to oversee different aspects of these complex deals.

The Competition Act serves as Canada’s primary antitrust law, administered by the Competition Bureau. This legislation applies to all M&A transactions and includes notification thresholds that trigger pre-merger review. What makes this particularly interesting is that the Commissioner of Competition has the statutory right to review and challenge any M&A transaction within one year after closing – giving regulators a much longer window than in many other jurisdictions.

The Investment Canada Act governs foreign investment in Canadian businesses, creating an additional layer of complexity for international acquirers. Non-Canadian buyers must obtain approval for acquisitions exceeding certain thresholds, with the government reviewing whether the investment is likely to be of “net benefit” to Canada. This review process can be lengthy and sometimes unpredictable, making timing a critical consideration.

Canada’s provincial securities regulators add another dimension to the regulatory landscape. Unlike the U.S. system with federal securities regulation, Canada has provincial securities regulators that must approve certain transactions involving public companies. This means dealing with multiple regulatory bodies, each with their own procedures and requirements.

Foreign investment rules in Canada are particularly strict in certain sectors. The government maintains specific restrictions on foreign investment in telecommunications, transportation, and cultural industries. These rules can significantly impact deal structure and feasibility, especially for strategic acquirers in these sectors.

The national security review process gives the Canadian government broad powers to review transactions that may affect national security. This authority includes the power to block deals entirely or impose conditions on approval, adding another layer of uncertainty to cross-border transactions.

Deal Structures and Timelines in Canada

Canadian M&A transactions typically use different structures than U.S. deals, reflecting the unique legal and regulatory environment. Understanding these structures is essential for choosing the right approach for your specific transaction.

Take-over bids are offers made directly to shareholders, often used for hostile transactions. Recent changes in 2016 significantly increased the minimum period during which a hostile bid must remain open from 35 days to 105 days. This extended timeline gives target companies more time to develop defensive strategies and can make hostile acquisitions more challenging and expensive.

The Plan of Arrangement is a court-supervised process similar to a U.S. merger, typically used for friendly transactions. This structure allows for more complex deal arrangements and provides court approval that can help resolve certain legal issues. The court supervision adds time to the process but can provide valuable legal certainty.

Early warning reporting requirements in Canada are more stringent than in many other jurisdictions. Canadian law requires public disclosure when an investor acquires 10% or more of a public company’s shares, with additional disclosure requirements for each 2% increase thereafter. This creates a more transparent environment but can also complicate acquisition strategies.

The Commissioner’s right to challenge transactions within one year of closing creates ongoing uncertainty even after deals close. This extended review period means that integration planning must account for the possibility of regulatory challenges well after the transaction has been completed.

Understanding these unique aspects is crucial for any cross-border M&A transaction involving Canadian entities. The interplay between federal and provincial regulations, combined with sector-specific restrictions and extended review periods, creates a complex environment that requires careful navigation.

Our Guide to public M&A in Canada provides comprehensive guidance for navigating these complex requirements and ensuring your transaction complies with all applicable Canadian laws and regulations.

Frequently Asked Questions about M&A Transactions

How long does an M&A deal usually take?

From first strategy meeting to integration can range from 6 months for a small private deal to 2 years for a regulated public transaction. Most of that time is consumed by due diligence, regulatory clearance, and post-closing integration.

What is the key difference between a merger and an acquisition?

A merger combines two firms into a new legal entity; an acquisition involves one company purchasing another’s shares or assets so the buyer survives and the target disappears or becomes a subsidiary. The choice affects taxes, liability, and required approvals.

Why is due diligence essential?

It verifies the seller’s claims, uncovers liabilities, and informs price and contract protections. Skimping here is the leading cause of post-closing surprises.

Conclusion

Successfully navigating the merger maze requires meticulous planning, strategic execution, and a deep understanding of the financial and legal intricacies involved. From initial valuation to post-merger integration, each step of an M&A transaction presents both opportunities and potential pitfalls that can make or break your deal.

The complexity of modern M&A transactions cannot be overstated. With due diligence processes involving at least 10 pages of categories, regulatory requirements spanning multiple jurisdictions, and integration challenges that can persist for years, these deals demand experienced guidance at every stage. It’s not just about buying or selling a company – it’s about orchestrating a complex dance of legal, financial, and operational elements that must all work in harmony.

Developing a clear strategic rationale before pursuing any deal sets the foundation for success. Too many companies get caught up in the excitement of a potential acquisition without truly understanding how it fits their long-term objectives. Investing in comprehensive due diligence might seem expensive and time-consuming, but it’s your best defense against the hidden surprises that can turn a promising deal into a costly mistake.

Structuring deals appropriately to achieve tax efficiency and risk mitigation requires careful consideration of your specific circumstances. Whether you choose a stock sale, asset purchase, or merger structure can have lasting implications for your business and your bottom line. Planning for integration from day one is equally crucial – the most beautifully executed transaction can still fail if you can’t successfully combine the two organizations afterward.

Maintaining regulatory compliance throughout the process protects you from costly delays and potential deal termination. Protecting your interests through appropriate representations, warranties, and indemnification gives you recourse when things don’t go as planned.

The statistics are sobering: research indicates that 50% of acquisitions are unsuccessful, often due to inadequate planning, insufficient due diligence, or poor integration execution. However, with proper guidance and careful execution, M&A transactions can create significant value and achieve strategic objectives. The key is approaching these deals with realistic expectations and comprehensive preparation.

For businesses in Indiana and beyond, partnering with experienced legal counsel is not just a recommendation—it’s a critical component of a successful deal. At Fritch Law Office PC, we understand the complexities of M&A transactions and provide the personalized, client-focused representation needed to steer these challenging waters successfully.

Whether you’re considering your first acquisition, planning a strategic exit, or exploring complex corporate restructuring, our team has the experience to guide you through every stage of the process. We’ve seen deals succeed and fail, and we know what it takes to protect your interests while achieving your strategic objectives. Every transaction is unique, and we take the time to understand your specific situation and goals.

The world of mergers and acquisitions doesn’t have to be overwhelming. With the right guidance and a clear understanding of the process, you can approach these transformative deals with confidence. The key is having experienced advocates in your corner who understand both the technical requirements and the human elements that make deals work.

Ready to discuss your M&A strategy? Contact our corporate lawyers for guidance.