Understanding the Importance of Estate Planning Financial Advice

Estate planning financial advice is essential for ensuring your assets are protected, your wishes are followed, and your loved ones are cared for after you’re gone. Planning for your estate isn’t just for the wealthy—it’s a crucial step for anyone who wants to maintain control over their legacy.

Key Elements of Estate Planning Financial Advice:

- Will & Trust Creation – Legal documents that direct how your assets are distributed

- Power of Attorney – Designates someone to make decisions if you become incapacitated

- Healthcare Directives – Communicates your medical care preferences

- Beneficiary Designations – Ensures assets transfer directly to intended recipients

- Tax Planning – Minimizes potential estate and inheritance taxes

Estate planning goes far beyond simply creating a will. It’s about making sure your financial affairs are in order and that your family is protected from unnecessary hardship during already difficult times. According to research, only about one-third of Americans have a will, and up to 90% of heirs choose to leave their benefactor’s original financial advisor when assets transfer, highlighting the importance of comprehensive planning.

The process works best when legal and financial professionals collaborate. Your estate plan should integrate with your overall financial strategy to ensure all aspects work together seamlessly.

Major life events like marriage, divorce, the birth of a child, or the death of a loved one should trigger a review of your estate plan. Even without such events, experts recommend reviewing your plan every 3-5 years to ensure it stays current with changing laws and circumstances.

I’m David Fritch, with over 40 years of experience as both an attorney and CPA, I’ve helped countless clients develop comprehensive estate planning financial advice strategies that protect their assets and provide peace of mind.

Why Estate Planning Matters at Every Stage of Life

Estate planning isn’t just something for retirees or the wealthy. It’s a fundamental piece of your financial puzzle that matters at every stage of life. Estate planning financial advice becomes important as soon as you own anything of value, have people who depend on you, or simply want control over what happens to your belongings.

“Many people think estate planning is only for the super-rich or the elderly,” says David Fritch, an experienced attorney with decades of practice in this field. “But the truth is, it’s for everyone who cares about what happens to their loved ones and their possessions.”

At its heart, estate planning gives you control over your legacy. It allows you to decide who receives your assets and when they receive them. It lets you name guardians for your children if something happens to you. It helps you plan for potential incapacity, minimizes taxes and expenses, protects your assets, and maintains your family’s privacy during difficult times.

The numbers tell a sobering story: only about one-third of Americans have created even a basic will. This means that most people are leaving crucial decisions about their assets to state intestacy laws rather than making these choices themselves. Even more concerning, research shows that up to 90% of heirs choose to leave their benefactor’s financial advisor when wealth transfers between generations, potentially disrupting carefully laid financial plans.

For Indiana residents, understanding the specifics of Estate Planning Indiana is particularly important, as state laws have unique aspects that affect how your estate is handled.

The Cost of Doing Nothing

Putting off estate planning might seem easier in the moment, but the long-term consequences can be devastating for those you leave behind.

Without proper planning, your state’s intestacy laws—not you—will determine who gets your assets. This process rarely aligns perfectly with what most people would choose for themselves. Your estate will likely go through probate, a public, court-supervised process that can tie up assets for months or even years, all while incurring legal fees that reduce what your heirs receive.

Family conflict often increases when there’s no clear roadmap. I’ve seen countless situations where relationships were permanently damaged because loved ones disagreed about what the deceased “would have wanted.” These disagreements add emotional strain during an already difficult time.

The financial impact can be substantial too. Without strategic tax planning, your estate might face unnecessary tax burdens that could have been avoided. And without advance healthcare directives, medical decisions might be made that don’t reflect your personal wishes.

One client shared with me: “I always thought estate planning was something I could deal with later. Then my neighbor passed unexpectedly at 42, leaving behind young children and no will. Watching his family steer that chaos while grieving was all the motivation I needed to get my own affairs in order.”

Estate planning isn’t about your death—it’s about protecting the people you love and the life you’ve built. It’s about peace of mind knowing that you’ve taken care of the important details so your family doesn’t have to guess what you would have wanted during what will already be a difficult time.

Estate Planning Financial Advice: Integrating Legal and Financial Strategies

Creating an effective estate plan isn’t just about legal documents—it’s about making sure your financial and legal strategies work together seamlessly. This is where estate planning financial advice truly shines, bringing together different expertise to protect what matters most to you.

Think of estate planning like building a house—you need both an architect (your attorney) and a general contractor (your financial advisor) to ensure everything comes together properly. When these professionals collaborate, you get a plan that not only follows the letter of the law but also maximizes financial benefits for you and your loved ones.

“Financial advisors add value not only by growing clients’ wealth but by helping plan its use during life and after death,” explains financial planning expert David Haughton. “Collaborating with attorneys is key to this process.”

The most successful estate plans involve a team approach with professionals who each bring unique expertise to the table. Your estate planning attorney creates the legal framework through wills, trusts, and powers of attorney. Meanwhile, your financial advisor ensures these documents align with your investments, retirement plans, and tax strategies. Tax professionals help minimize tax burdens, while insurance specialists recommend appropriate coverage to protect your family.

At Fritch Law Office PC, we work closely with our clients’ financial advisors to create harmony between legal and financial strategies. This teamwork helps prevent common mistakes like trusts that never get funded or beneficiary designations that conflict with your will.

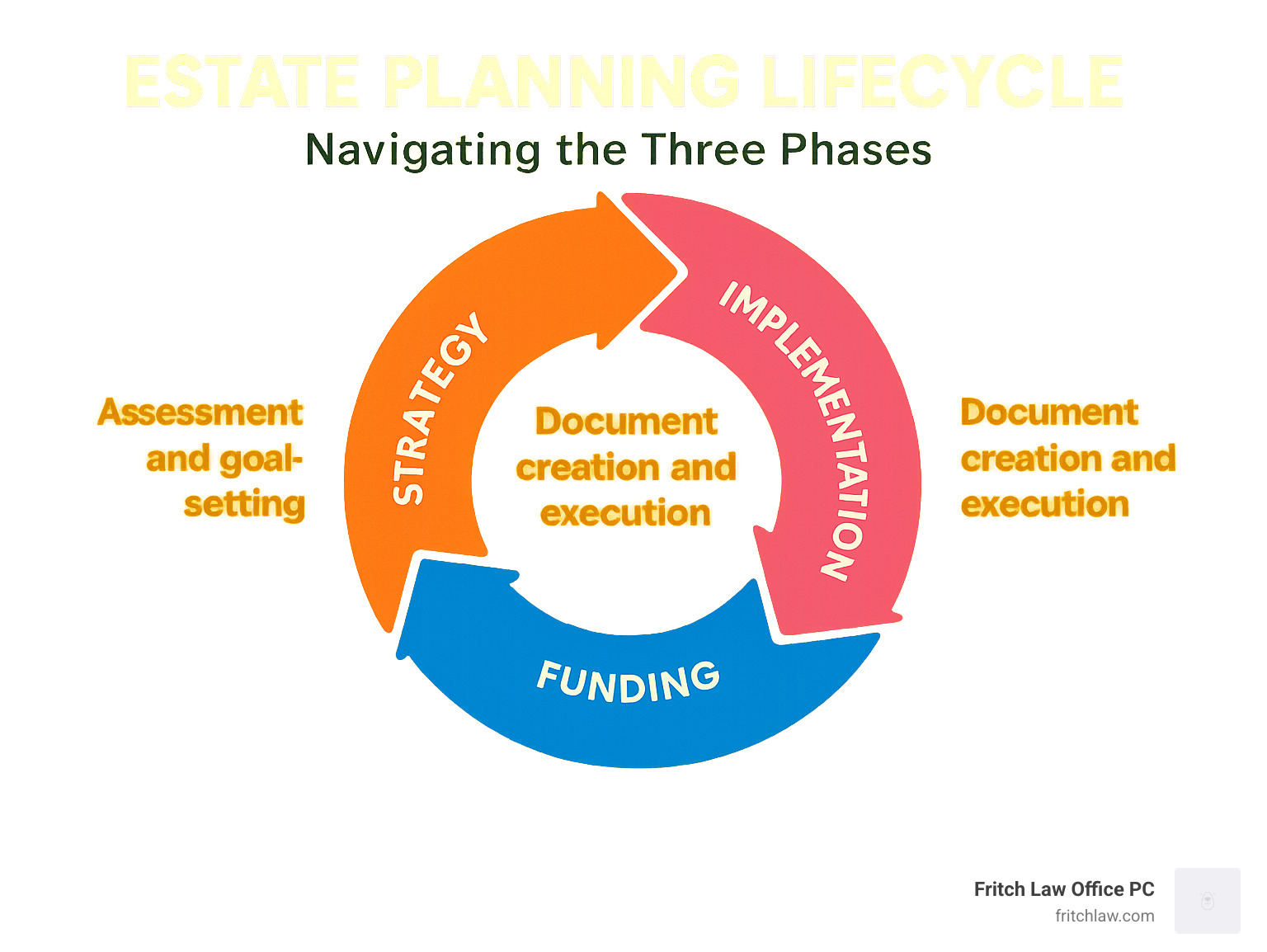

Estate planning typically unfolds in three phases:

1. Strategy Phase: Here we identify your goals, assess your assets, and determine the right legal structures for your situation.

2. Implementation Phase: This is when we create and execute all the necessary legal documents.

3. Funding Phase: Often overlooked but critical—ensuring assets are properly titled and beneficiary designations align with your overall plan.

Each phase works best when both legal and financial professionals contribute their expertise. For instance, your financial advisor might suggest tax-efficient gifting strategies during the planning phase, while we ensure these strategies are properly documented in your estate plan.

Estate Planning Financial Advice for Young Families

If you’re a young family with children, estate planning financial advice becomes especially important, even if you don’t have substantial assets yet.

Guardianship designations top the priority list for parents of minor children. Without naming guardians in your will, courts will decide who raises your children if something happens to both parents—a thought no parent wants to consider, but responsible planning requires it.

Life insurance plays a crucial role for young families too. The right coverage can replace lost income, pay off your mortgage and other debts, and fund future expenses like your children’s college education. Working with both insurance specialists and estate planning attorneys ensures these policies integrate properly with your overall plan.

Don’t overlook the importance of an emergency fund as part of your estate plan. Having 3-6 months of expenses readily available ensures your family has immediate funds while your estate is being settled, which can take time even with perfect planning.

“We often see young parents who assume they don’t need estate planning because they don’t have significant assets,” notes an experienced advisor. “They don’t realize that guardianship designation alone is reason enough to create an estate plan.”

For more specific guidance on estate planning for families in Indiana, visit our page on Estate Planning Lawyer Greenwood Indiana.

Estate Planning Financial Advice for Retirees

As you enter your retirement years, your estate planning needs evolve significantly. Retirees face unique challenges that require specialized estate planning financial advice.

Managing Required Minimum Distributions (RMDs) from retirement accounts becomes a key consideration for those over 73. These mandatory withdrawals can significantly impact your tax situation and estate plan. A coordinated approach between your financial advisor and estate planning attorney can help ensure these distributions align with your broader goals.

Charitable giving often becomes more important in retirement years. Vehicles like donor-advised funds (DAFs) allow you to make tax-deductible contributions now, grow the funds tax-free, and recommend grants to charities over time. This approach can be particularly useful if you want to establish a charitable legacy without the complexity of a private foundation.

Long-term care planning is another critical element for retirees. Whether through insurance, asset protection strategies, or Medicaid planning, addressing potential care needs protects both your quality of life and the legacy you hope to leave behind.

Legacy planning in retirement isn’t just about financial assets—it’s also about passing down values, stories, and meaningful possessions to future generations. We can help you create a comprehensive approach that addresses both the tangible and intangible aspects of your legacy.

For more detailed information about estate planning services in the Indianapolis area, visit our page on Estate Planning and Probate Attorney Indiana Indianapolis.

Learn more about our full range of estate planning services at Estate Planning, or if you’re looking for financial planning assistance to complement your legal strategy, consider reaching out to Find an advisor.

Key Components of a Comprehensive Estate Plan

When it comes to protecting your future and your loved ones, a solid estate plan isn’t just nice to have—it’s essential. Think of a comprehensive estate plan as a safety net that catches all aspects of your life and legacy. Let’s explore the key pieces that work together to create this protection.

Wills

At the heart of most estate plans sits the humble yet powerful will. This foundational document does far more than just distribute your belongings.

“A will is like a roadmap for your loved ones,” explains an estate planning professional. “Without one, the state essentially creates that roadmap for you—and it rarely matches what you would have wanted.”

Your will enables you to name an executor (the person who’ll handle your affairs), designate guardians for your children, specify how your assets should be distributed, and even create testamentary trusts. Without this crucial document, state laws—not your wishes—determine what happens to everything you’ve worked for.

Trusts

While wills handle the basics, trusts offer improved control and privacy. Estate planning financial advice often includes trust recommendations based on your specific situation:

Revocable living trusts let you maintain control of your assets during life while providing for their management if you become incapacitated. Plus, assets properly held in trust avoid the public probate process after death.

Irrevocable trusts offer asset protection and potential tax benefits, though you generally can’t change them once established.

Special needs trusts protect beneficiaries who receive government benefits, ensuring they have supplemental resources without losing eligibility.

Charitable trusts help you support causes you care about while potentially reducing your tax burden.

Powers of Attorney

Life is unpredictable, and powers of attorney prepare for times when you might be unable to handle your own affairs:

A financial power of attorney designates someone you trust to manage your finances if you can’t do so yourself—paying bills, managing investments, or handling other financial matters.

A healthcare power of attorney (sometimes called a healthcare proxy) names a person to make medical decisions on your behalf when you’re unable to communicate your wishes.

Healthcare Directives

Healthcare directives (or living wills) document your preferences for medical treatment if you become incapacitated. These documents address critical questions about life-sustaining treatments, pain management preferences, organ donation desires, and other end-of-life care decisions.

Having these documents in place spares your loved ones the agonizing uncertainty of guessing what you would want during an already difficult time.

Digital Asset Planning

Comprehensive estate planning financial advice must include provisions for your online life:

“Most people don’t realize that without specific authorization, their loved ones may not be able to legally access their digital accounts after death,” notes a digital estate planning specialist.

Your plan should address online accounts, cryptocurrencies, digital photos and documents, social media profiles, and any intellectual property you own online. Without proper planning, these assets could be lost forever or create unnecessary complications for your family.

Beneficiary Designations

Many of your most valuable assets—retirement accounts, life insurance policies, and certain bank accounts—pass directly to named beneficiaries, completely bypassing your will or trust. These designations actually override instructions in your will, making them a critical component of your estate plan that requires regular review.

Funding Your Trust the Right Way

Creating a trust is only half the battle—funding it properly is where many people stumble. An unfunded trust is essentially an empty vault that provides no protection.

“Unfunded trusts are one of the most common estate planning mistakes we see,” shares a trust administration expert. “People spend time and money creating a trust but then fail to transfer their assets into it.”

Proper trust funding involves retitling assets from your individual name to your trust’s name, updating beneficiary designations to align with your trust strategy, using transfer-on-death designations when appropriate, and regularly reviewing new assets to ensure they’re properly titled. Skip these steps, and your assets might still wind up in probate—defeating a primary purpose of having a trust in the first place.

Protecting Loved Ones with Special Needs

For families with special needs dependents, thoughtful estate planning becomes even more crucial. Without proper planning, an inheritance could inadvertently disqualify your loved one from essential government benefits.

Special needs planning typically centers around specialized trusts that hold assets for your loved one’s benefit without counting against eligibility for programs like Medicaid and Supplemental Security Income. These can be complemented with ABLE accounts—tax-advantaged savings accounts that don’t affect certain federal benefits.

Many families also create a detailed letter of intent providing information about their loved one’s routines, needs, and preferences to guide future caregivers. And of course, guardianship considerations are paramount—determining who will make personal and financial decisions when you no longer can.

“When planning for a loved one with special needs, the goal is to improve their quality of life while preserving their eligibility for benefits,” explains a special needs planning specialist. “A properly structured special needs trust can accomplish both objectives.”

At Fritch Law Office PC, we understand that creating a comprehensive estate plan might seem overwhelming. That’s why we guide you through each component, ensuring nothing is overlooked in protecting what matters most to you.

Common Pitfalls and How to Avoid Them

Estate planning is filled with potential missteps that can derail even the best intentions. Understanding these common pitfalls can save your family significant heartache and expense down the road.

Outdated Documents

Life doesn’t stand still, and neither should your estate plan. Many people create their documents and then file them away, never to be seen again. This “set it and forget it” approach can lead to serious problems.

“I had a client whose ex-spouse received a substantial life insurance payout because he never updated his beneficiary designation after their divorce,” shares a financial advisor we work with. “His current family received nothing from that policy, despite what his will stated.”

Your estate plan should evolve as your life does. Major life events like marriage, divorce, birth of children, death of beneficiaries, or significant financial changes should trigger an immediate review. Even without these events, your documents can become outdated due to changes in tax laws or a move to a different state.

Missing or Inconsistent Beneficiary Designations

One of the most common mistakes we see involves beneficiary designations. Many people don’t realize that these designations on retirement accounts, life insurance policies, and transfer-on-death accounts override what’s written in your will or trust.

Problems frequently arise when:

- You forget to name backup (contingent) beneficiaries

- Your beneficiary designations contradict your will or trust

- You directly name minors as beneficiaries without proper trust provisions

- You fail to update designations after major life changes

Taking time to review all your beneficiary designations can prevent these inconsistencies and ensure your assets go where you intend.

Incapacity Planning Gaps

While many people focus on what happens after death, they often neglect planning for potential incapacity. Without proper healthcare directives and financial powers of attorney, your family may face court proceedings to gain authority to make decisions on your behalf.

“The most heart-wrenching situations I’ve seen involve families who must petition for guardianship of a loved one who could have easily avoided this with proper incapacity planning,” notes a colleague who specializes in elder law.

Comprehensive incapacity planning should include provisions for healthcare decisions, financial management, and potential long-term care needs.

Digital Legacy Oversights

In our increasingly digital world, failing to address your online presence can create significant headaches for your loved ones. From social media accounts to cryptocurrency and digital photos, your digital assets need specific planning.

Without proper documentation and legal authorization, your family may be unable to access your online accounts, potentially losing valuable or sentimental digital property forever. Consider creating a digital asset inventory and including specific language in your estate planning documents to address these modern concerns.

How Often Should You Update Your Plan?

We generally recommend reviewing your estate plan every 3-5 years, even if nothing significant has changed in your life. This periodic review ensures your plan stays aligned with your goals and current laws.

However, certain life events should trigger an immediate review:

Family changes like marriages, divorces, births, and deaths can dramatically affect how you want your assets distributed. Financial changes such as receiving an inheritance, selling a business, or significant market fluctuations might necessitate adjustments to your strategy. Health changes, relocations to different states, and legal or tax law revisions should also prompt a review of your documents.

The estate plans that fail are typically those that were created and then forgotten. Life evolves, and your estate plan should too.

DIY vs Professional Help

With online legal services promising quick and inexpensive estate documents, many people are tempted to handle their planning themselves. While this approach might work for very simple situations, it often creates more problems than it solves.

DIY estate planning is a bit like performing your own dental work – possible in theory, but risky in practice. The main concerns include:

State-specific requirements that vary significantly across jurisdictions and may not be fully addressed in generic templates. Technical execution requirements that, if not followed precisely, can invalidate your documents entirely. Integration with your broader financial strategy is typically missing from DIY approaches.

For situations involving family businesses, blended families, special needs dependents, or substantial assets, professional guidance becomes even more critical. At Fritch Law Office PC, we’ve helped many clients correct problematic DIY documents before they caused real damage.

“The problem with DIY estate planning isn’t that the documents are always wrong—it’s that you won’t know they’re wrong until it’s too late to fix them,” as one of our colleagues aptly puts it.

Estate planning financial advice works best when legal and financial professionals collaborate to create a comprehensive strategy that addresses both the legal documents and the financial structures that support them. This integrated approach helps ensure that your plan actually works when your family needs it most.

Expert Roundup: Pro Tips from Advisors, Attorneys, and Tax Pros

We’ve gathered insights from experienced professionals across disciplines to provide you with comprehensive estate planning financial advice. Here’s what these experts want you to know:

From Estate Planning Attorneys:

“The biggest mistake I see is people waiting until they think they’re ‘wealthy enough’ to need an estate plan. Everyone needs basic documents like a will, powers of attorney, and healthcare directives—regardless of net worth.”

“Trust funding is where many estate plans fail. Creating a beautiful trust document means nothing if your assets aren’t properly titled in the name of the trust.”

“Don’t forget about digital assets. Make sure your estate plan includes provisions for accessing and managing your online accounts, digital photos, and other electronic assets.”

From Financial Advisors:

“Review beneficiary designations annually. These designations override what’s in your will, and outdated designations are one of the most common causes of assets going to unintended recipients.”

“Consider the tax implications of your inheritance plan. Sometimes the ‘fair’ approach of dividing assets equally among children isn’t the most tax-efficient strategy.”

“Don’t neglect long-term care planning as part of your estate strategy. The cost of extended care can quickly deplete an estate if not properly planned for.”

From Tax Professionals:

“The federal estate tax exemption is scheduled to decrease significantly at the end of 2025 unless Congress acts. If your estate is near the current exemption amount, now is the time to consider gifting strategies.”

“Many people overlook state estate taxes. Even if your estate isn’t large enough to trigger federal estate tax, it might be subject to state estate tax depending on where you live.”

“Retirement accounts have specific tax rules when inherited. The SECURE Act eliminated the ‘stretch IRA’ for many beneficiaries, making it crucial to revisit how you plan to pass these assets.”

Top Tax-Smart Giving Strategies

Strategic giving can reduce your taxable estate while supporting causes you care about. Here are some tax-smart giving strategies recommended by experts:

-

Annual Exclusion Gifts: You can give up to $17,000 (as of 2023) per recipient per year without using any of your lifetime gift tax exemption. For married couples, this amount doubles to $34,000 per recipient.

-

Donor-Advised Funds (DAFs): These charitable giving vehicles allow you to make a tax-deductible contribution now, invest the funds for tax-free growth, and recommend grants to charities over time.

-

Qualified Charitable Distributions (QCDs): If you’re over 70½, you can direct up to $100,000 annually from your IRA to qualified charities, satisfying required minimum distributions without increasing your taxable income.

-

Charitable Remainder Trusts (CRTs): These trusts provide you or your beneficiaries with income for a period of time, after which the remaining assets go to charity. They can provide an immediate partial tax deduction and reduce capital gains taxes.

-

Charitable Lead Trusts (CLTs): The opposite of CRTs, these trusts provide income to charity for a period of time, after which the remaining assets go to your beneficiaries, potentially with reduced gift or estate taxes.

“The key is to align your charitable goals with your overall financial and estate plan,” advises a philanthropic planning specialist. “The right giving strategy depends on your specific situation, including your age, income needs, and tax circumstances.”

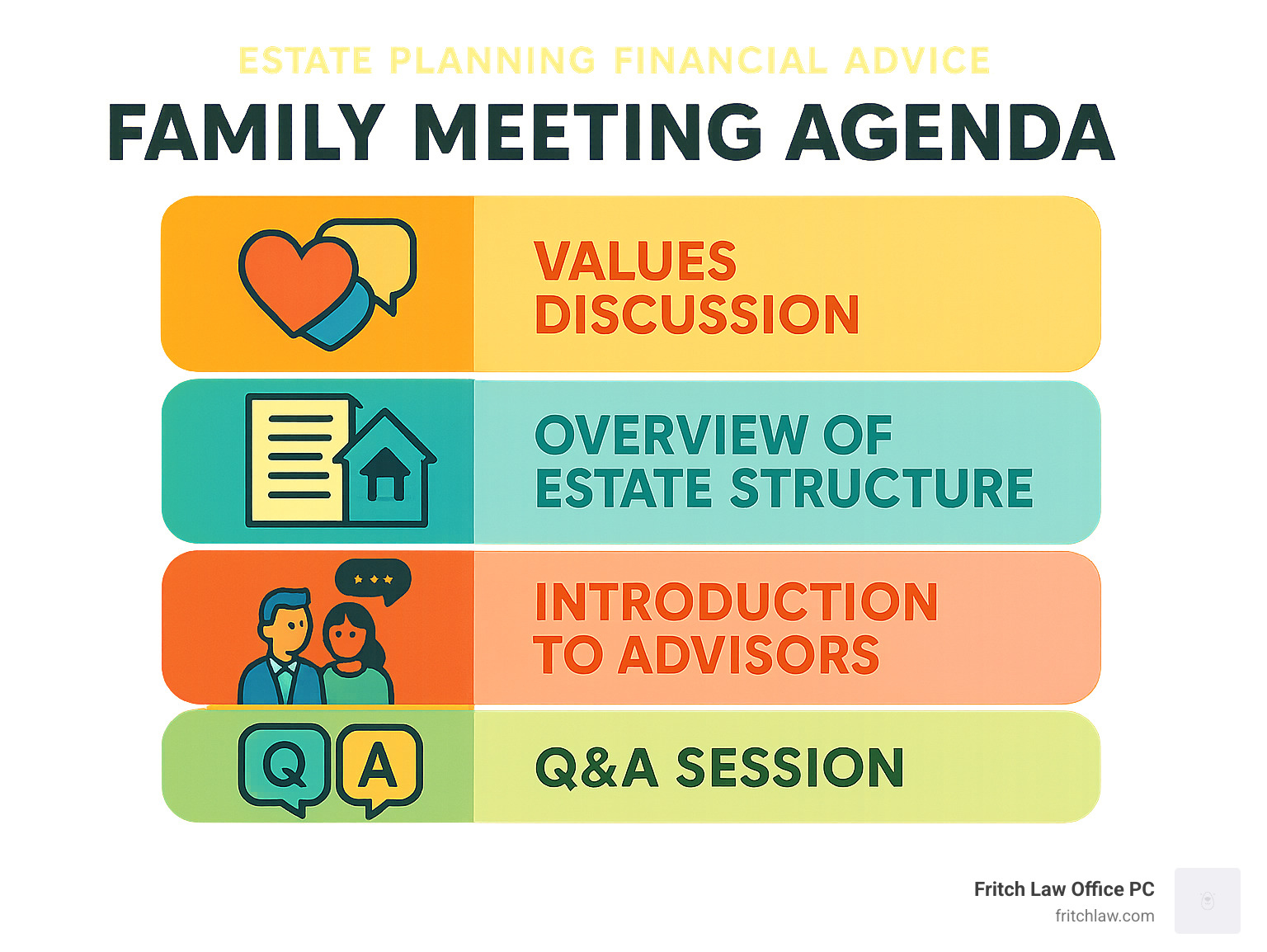

Communicating Your Wishes to Family

One often overlooked aspect of estate planning is communicating your intentions to family members. Clear communication can prevent confusion, conflict, and hurt feelings later on.

“Many family disputes after death could have been avoided with a simple conversation during life,” observes a family wealth counselor. “When heirs understand not just what decisions were made but why, they’re much more likely to accept and respect those decisions.”

Effective ways to communicate your estate plan include:

-

Family meetings: Gathering family members to discuss your overall plans and values (though specific financial details can remain private if preferred).

-

Letters of intent: Writing personal letters to explain decisions that might otherwise be misunderstood.

-

Ethical wills: Creating a non-legal document that passes down your values, life lessons, and wishes for future generations.

-

Gradual involvement: Including adult children in meetings with your advisors to familiarize them with your planning team.

“The way you communicate your estate plan is almost as important as the plan itself,” notes a family dynamics expert. “Approach these conversations with empathy, understanding that what seems perfectly logical to you might still trigger emotional responses from family members.”

Frequently Asked Questions about Estate Planning Financial Advice

What is the difference between estate planning and financial planning?

Many people wonder how estate planning differs from financial planning. Though they’re closely related, they serve distinct purposes in your overall wealth management strategy.

Financial planning is all about helping you reach your money goals while you’re alive. Think of it as your roadmap for building and managing wealth during your lifetime. This typically includes creating a budget that works for your lifestyle, saving for major purchases like a home or college education, managing your investments wisely, preparing for a comfortable retirement, and protecting yourself with appropriate insurance coverage.

Estate planning, on the other hand, focuses on what happens to everything you’ve built when you’re no longer able to manage it yourself—either due to incapacity or death. This involves creating legal documents like wills and trusts, appointing trusted individuals through powers of attorney, setting up beneficiary designations, developing strategies to minimize taxes when transferring wealth, and naming guardians for your children if needed.

As one of our clients recently shared, “I always thought financial planning and estate planning were the same thing. Now I understand that my financial plan helped me build wealth, while my estate plan ensures that wealth benefits my family the way I intend.”

The two disciplines work hand-in-hand. The most comprehensive approach is to coordinate your financial and estate planning so all aspects of your wealth management work together seamlessly.

How can I avoid probate and keep my affairs private?

Privacy concerns often lead people to ask about avoiding probate—that court-supervised process of validating a will and distributing assets. Beyond being public, probate can also be time-consuming and potentially costly.

Fortunately, there are several effective strategies to keep your affairs private by bypassing probate:

Creating a revocable living trust is perhaps the most comprehensive approach. When you properly transfer assets to your trust during your lifetime, those assets can pass directly to your beneficiaries without court involvement. Many clients appreciate that trusts offer privacy while still giving them complete control during their lifetime.

Other effective probate-avoidance tools include holding property in joint ownership with right of survivorship, using beneficiary designations on retirement accounts and life insurance policies, setting up payable-on-death designations for bank accounts, and thoughtful lifetime gifting (though be mindful of potential tax implications).

“After watching my neighbor’s family endure a lengthy, public probate process, I decided to create a living trust,” explains a Fritch Law Office client. “Knowing my affairs will remain private gives me tremendous peace of mind.”

At Fritch Law Office PC, we help clients understand which probate-avoidance strategies make the most sense for their unique situation and family dynamics.

Which life events should trigger an immediate review of my estate plan?

Life doesn’t stand still, and neither should your estate plan. Certain key events should prompt you to dust off those documents and schedule a review with your estate planning financial advice team.

Marriage or divorce fundamentally changes your family structure and how property is owned. Either event should trigger an immediate review to ensure your estate plan reflects your current wishes and relationships.

The birth or adoption of children or grandchildren might necessitate naming guardians or adjusting how your assets will eventually be distributed. These joyful events often inspire people to think more seriously about their legacy.

The death of anyone named in your estate plan—whether a spouse, beneficiary, executor, or trustee—creates an immediate need to update your documents. Failing to replace a deceased executor, for example, could leave your estate without clear direction.

Significant financial changes like buying or selling a business, receiving an inheritance, or taking on substantial debt can dramatically alter your estate planning needs and strategies.

Moving to a different state matters because estate laws vary significantly across state lines. What worked perfectly in Illinois might not be optimal in Indiana.

Major tax law changes may require adjustments to your estate planning strategies to maintain tax efficiency. The scheduled reduction of the federal estate tax exemption in 2026 is prompting many to review their plans now.

A serious health diagnosis often creates urgency around completing or updating an estate plan. While difficult to contemplate, addressing these matters brings tremendous peace of mind during challenging times.

“I tell clients to think of their estate plan as a living document that grows and changes as their life does,” says an advisor who works closely with Fritch Law Office. “The best estate plans evolve alongside the families they protect.”

Regular reviews of your estate plan—ideally every 3-5 years—help ensure it continues to reflect your current wishes and circumstances, even when major life events haven’t occurred.

Conclusion

Navigating estate planning financial advice isn’t just about creating documents—it’s about crafting a meaningful legacy that protects the people and causes you care about most. When legal, financial, and tax considerations work in harmony, you create a plan that truly serves your wishes and safeguards your loved ones.

Life’s journey is full of changes—marriages, births, career shifts, and relocations. Your estate plan should evolve alongside these milestones, adapting to new circumstances and opportunities. This isn’t a one-and-done task but rather an ongoing conversation between you, your loved ones, and your professional advisors.

At Fritch Law Office PC, we see ourselves as partners in your legacy journey. Our team in Jasper, Indiana brings decades of experience helping families create personalized plans that reflect their unique values and goals. We believe that thoughtful estate planning gives you something priceless: peace of mind knowing you’ve taken care of the important details.

The most successful estate plans don’t happen in isolation. They involve clear communication with family members, regular reviews with professional advisors, and adjustments as laws and life circumstances change. By staying proactive, you ensure your plan continues to serve its intended purpose.

Whether you’re just beginning to explore estate planning or need to update an existing plan, we’re here to guide you through each step with clarity and care. Our approach focuses on understanding your unique situation and helping you make informed decisions that align with your values.

For more information about our comprehensive estate planning services, visit our Estate Planning page or reach out to our office directly. We welcome the opportunity to help you secure your legacy and provide for the people who matter most in your life.

The road to a well-crafted estate plan begins with a single step. We’re ready when you are.