Understanding Indiana’s Non-Probate Claims System

Indiana non probate claims law governs how creditors can pursue debts against assets that pass outside of traditional probate. If you’re looking for quick answers about this topic, here’s what you need to know:

| Key Aspect | Indiana Non-Probate Claims Law |

|---|---|

| Definition | Assets that transfer at death without going through probate court |

| Examples | Revocable trusts, TOD deeds, joint accounts with survivorship rights |

| Excluded Assets | Life insurance, retirement accounts, tenancy by entirety property |

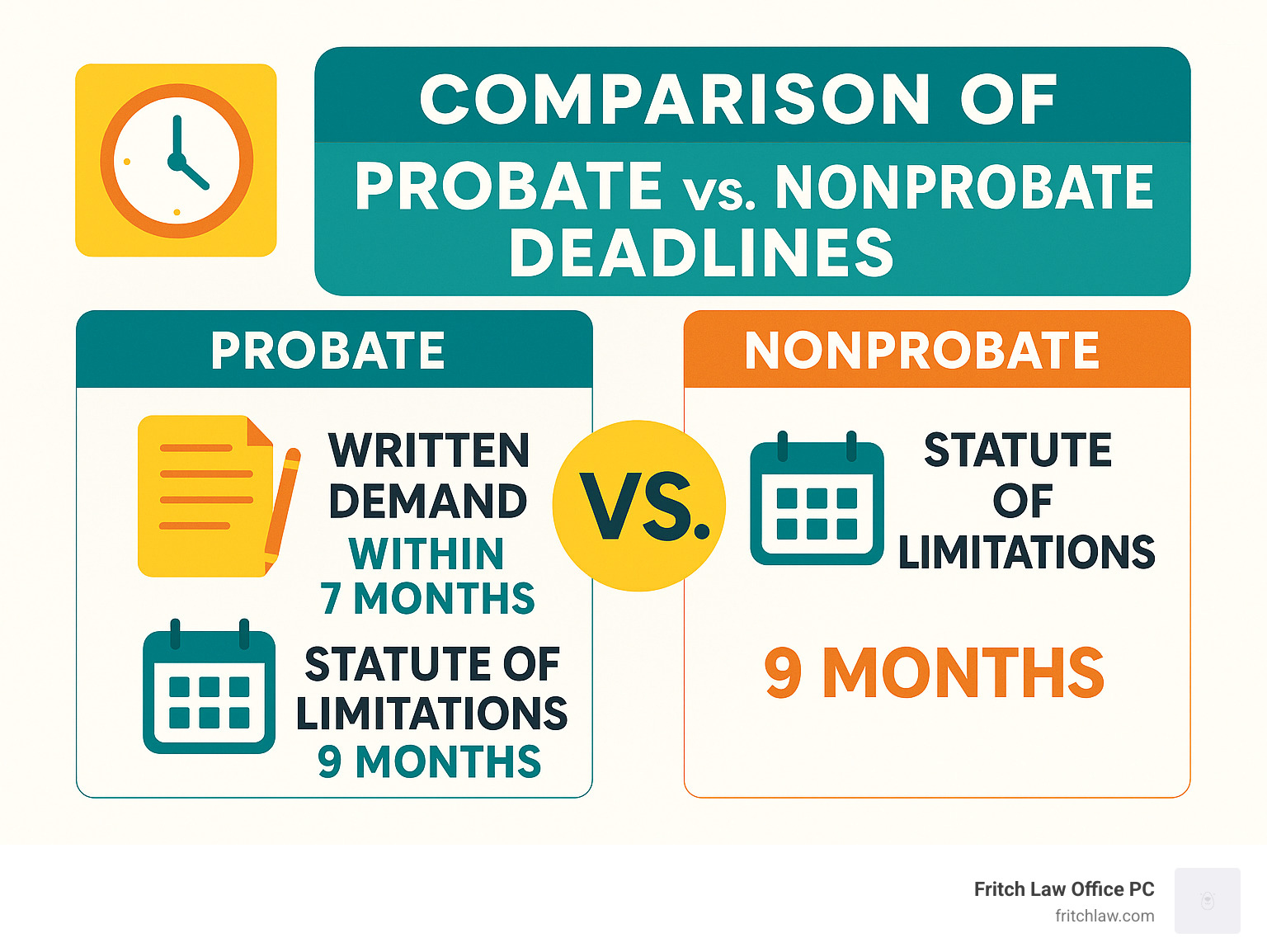

| Creditor Deadline | Claims must be filed within 9 months of death |

| Required Process | File claim in probate, serve transferees within 5 months, submit written demand to personal representative within 7 months |

When someone passes away in Indiana, not all of their assets go through the probate court process. Many valuable assets—like jointly owned property, revocable trust assets, and accounts with beneficiary designations—transfer automatically to new owners without court supervision. This creates a potential problem: How can creditors collect what they’re owed if the assets bypass probate?

That’s where Indiana non probate claims law comes into play. Under Indiana Code Title 32, Article 17, Chapter 13, specific procedures allow creditors to reach certain non-probate assets to satisfy legitimate debts, while still providing important protections for beneficiaries.

Understanding these laws is crucial for both creditors seeking payment and beneficiaries who’ve received assets outside of probate. The rules include strict deadlines, specific procedural requirements, and important limitations on which assets can be reached.

I’m David Fritch, and with over 40 years of experience practicing law in Indiana, I’ve guided numerous clients through the complexities of Indiana non probate claims law, helping both creditors and beneficiaries steer these challenging legal waters effectively.

Indiana non probate claims law word guide:

– does indiana law require estate to go through probate

– indiana law executor probate

– indiana probate law small estate

What Counts as a Nonprobate Transfer in Indiana?

When someone passes away in Indiana, you might be surprised to learn that many valuable assets never go through probate court at all. These “nonprobate transfers” move directly to new owners when someone dies, following instructions the person set up during their lifetime.

Definition under IC 32-17-13-1

Under Indiana non probate claims law, specifically Indiana Code 32-17-13-1, nonprobate transfers have three key elements:

- The transfer takes effect only when the person dies

- The person’s last legal residence was in Indiana

- The person had complete control to change their mind, take back the asset, or name different beneficiaries right up until their death

This “unrestricted power” test is what really matters. If Mom could have changed her mind about who gets her lake cottage or emptied that joint bank account while she was alive, it’s likely a nonprobate transfer that might face creditor claims later.

Assets Included by Statute

Let’s talk about what actually counts as nonprobate property in Indiana. Your bank accounts with “payable on death” designations? Those are nonprobate transfers. That house you put in a revocable living trust? Also a nonprobate transfer.

Indiana non probate claims law specifically includes:

Bank accounts where you’ve named someone to receive the money when you die, revocable trust assets you controlled during life, real estate with transfer-on-death deeds, jointly owned property with survivorship rights, vehicles with beneficiary designations, and even boats or other watercraft with transfer-on-death titles.

For example, if you and your sister share a bank account with “joint with right of survivorship” language, when you pass away, that money becomes hers automatically—no probate needed. But your creditors might still have rights to that money in certain situations.

Statutory Exclusions You Must Know

Not everything that bypasses probate can be touched by creditors. Indiana non probate claims law creates important safe harbors for certain assets:

Your life insurance death benefits paid to named beneficiaries are generally protected from your creditors. The same goes for your IRA, 401(k), and other retirement accounts. Annuities typically can’t be touched either.

Real estate owned by married couples as “tenancy by the entirety” gets special protection too. This unique form of ownership means when one spouse dies, the survivor automatically owns the entire property—and it’s generally shielded from the deceased spouse’s creditors.

These exclusions matter tremendously for family financial security. If your husband named you beneficiary on his $500,000 life insurance policy, that money is typically safe from his business debts or medical bills, even if there’s not enough money in the probate estate to pay everyone.

It’s worth noting that in 2022, Indiana increased its small estate threshold to $100,000, allowing more families to use simplified procedures rather than formal probate. This change affects how nonprobate transfers interact with the overall estate settlement process.

Understanding what counts as a nonprobate transfer—and what doesn’t—is the crucial first step in navigating Indiana’s probate thresholds and protecting your rights, whether you’re receiving assets or trying to collect a legitimate debt.

Creditor Rights and Deadlines Under Indiana Non Probate Claims Law

When someone passes away owing money, creditors face a ticking clock to collect from assets that bypassed probate. Whether you’re a creditor trying to collect what you’re owed or a beneficiary who received assets outside probate, understanding these deadlines isn’t just important—it’s essential.

Three Critical Filing Windows

The indiana non probate claims law creates a strict timeline that doesn’t forgive missed deadlines:

First, there’s the 5-month service rule. Within five months of death, creditors must serve a copy of their claim on each person who received nonprobate assets. This isn’t optional—it’s your first crucial deadline.

Next comes the 7-month written demand. Within seven months after death, creditors must deliver a formal written request to the personal representative asking them to pursue those nonprobate transferees. Think of this as your official “please take action” notice.

Finally, the 9-month statute of limitations serves as the ultimate cutoff. All claims that could be barred under Indiana Code 29-1-14-1(a) will be permanently blocked if not filed within nine months after death—even for nonprobate transfers. This deadline is unforgiving and applies whether or not a probate estate has been opened.

Miss any of these windows, and you might find yourself permanently unable to collect, no matter how legitimate your claim.

What Information Goes in a Creditor’s Written Demand?

Your written demand to the personal representative isn’t just a casual request—it needs specific details to be valid under indiana non probate claims law. You must include the estate’s cause number (the court file number), a clear statement of your claim as filed in the estate, a description of the nonprobate transfer instrument, and complete names and addresses of all nonprobate transferees.

Leaving out any of these elements could render your demand ineffective. For instance, if you forget to include the transferees’ addresses, the personal representative might rightfully reject your demand as incomplete. Details matter tremendously here.

Statute of Limitations and Tolling Rules

While the nine-month deadline appears absolute, a few special rules create limited exceptions:

The personal representative enjoys a 30-day immunity period after receiving your written demand to decide whether to pursue nonprobate transferees. During this time, you can’t bypass them and file directly.

If your claim is allowed by the personal representative or ordered paid by the court, you gain a 90-day extension after that final allowance to commence proceedings against nonprobate transferees. This gives you a little breathing room once your claim is validated.

Government claims, particularly Medicaid estate recovery, sometimes play by different rules with potentially longer deadlines. If you’re dealing with a government claim, you’ll want specialized advice.

And while not directly related to nonprobate claims, probate proceedings generally must begin within a three-year probate cap after death. This overarching deadline affects the entire estate administration process.

These timing requirements can feel overwhelming, especially during an already stressful time. At Fritch Law Office, we’ve guided countless clients through these complex deadlines, helping both creditors and beneficiaries understand their rights and responsibilities under indiana non probate claims law. The clock starts ticking immediately upon death—not when you find the death or when probate begins—making prompt action essential.

Step-by-Step Procedure to Enforce Claims Against Nonprobate Transferees

Navigating the process of enforcing claims against nonprobate transfers can feel like walking through a legal maze. Let me guide you through each step with clarity so you know exactly what to expect under Indiana non probate claims law.

First things first – all claims must begin in the probate estate itself. Even when you’re ultimately trying to reach assets that transferred outside probate, you must file your claim with the estate. This establishes your standing as a legitimate creditor.

Within five months of the person’s death, you’ll need to serve a copy of your claim on each nonprobate transferee you’re seeking recovery from. Don’t delay on this step – it’s a strict deadline!

By the seven-month mark after death, you must deliver a formal written demand to the personal representative. This document essentially asks them to take action against the nonprobate transferees on your behalf.

Once your demand is delivered, the personal representative has 30 days to decide whether they’ll pursue the matter. During this waiting period, you can’t take independent action – the ball is in their court.

If the personal representative decides not to act (or simply doesn’t respond within those 30 days), you gain the right to bring proceedings yourself in the estate’s name. This is an important protection for creditors facing uncooperative estate representatives.

When filing your action, you have several venue options. You can file in any Indiana county where: the nonprobate transfer occurred, where the transferee lives, or where the probate case is already pending. This flexibility can be strategically valuable.

If No Probate Estate Exists

“What if nobody opened a probate estate?” This is a common question, and fortunately, Indiana non probate claims law doesn’t leave creditors stranded.

As a creditor, you have the right to petition the court to open an estate yourself and request appointment of a personal representative. This gives you a pathway to pursue your claim even when family members haven’t initiated probate.

If the estate qualifies as a small estate (currently under $100,000 in Indiana), different procedures may apply. The small estate affidavit process creates some unique challenges for creditors that require careful navigation.

Without an existing probate case, your venue selection becomes especially important. You’ll need to carefully consider where to file based on asset locations or where the transferees reside.

Even without an open probate estate, that nine-month statute of limitations is still ticking. You can’t extend your time simply because no one opened a probate estate.

Personal Representative Fails to Act—Now What?

When a personal representative receives your proper written demand but doesn’t take action within 30 days, you gain important rights as a creditor under Indiana non probate claims law.

You can step into their shoes and commence proceedings against the nonprobate transferee in the estate’s name. This prevents personal representatives from simply ignoring legitimate creditor demands.

There are limits, however. Your recovery is capped at the amount of your claim plus any costs incurred. You won’t be able to recover more than what you’re actually owed.

Be aware that you may have to cover your own attorney fees if the personal representative had valid reasons for declining to bring the action. This discourages frivolous claims while still protecting legitimate creditors.

Serving and Collecting From Multiple Transferees

Many estates distribute assets to multiple beneficiaries through nonprobate transfers. The law has specific provisions for these situations.

Multiple transferees can be jointly liable for your claim. This means you potentially could recover from any or all of them, depending on the circumstances.

If one transferee pays more than their fair share, they can seek contribution from other transferees. This prevents one beneficiary from unfairly bearing the entire burden.

Settling with one transferee doesn’t necessarily release others from liability. Each case has its own dynamics, and the release mechanics depend on the specific situation and agreement terms.

For example, if a parent transferred assets to three children through nonprobate means, a creditor might recover from any or all of them. The children would then need to sort out the proportional responsibility among themselves.

Understanding these procedures isn’t just important for creditors – beneficiaries who’ve received nonprobate transfers should also be familiar with these rules to protect their interests and prepare for potential claims.

Liability Hierarchy, Apportionment, and Transferee Defenses

When dealing with creditor claims after a loved one passes, it helps to understand who’s responsible for what under Indiana non probate claims law. The system isn’t random—it follows a carefully designed order of operations that balances the interests of creditors, family members, and beneficiaries.

Priority Between Probate and Nonprobate Property

Indiana law creates a clear pecking order for paying debts:

First, creditors must look to the probate estate assets. Think of this as the first line of defense—all assets passing through probate must be used up before nonprobate transfers can be touched. This makes sense when you consider that probate assets are already under court supervision.

Within the probate estate itself, there’s another hierarchy at work. Administration costs (including reasonable funeral expenses) get paid first, followed by family allowances that protect surviving spouses and dependent children. Only after these priority items are handled do general creditors get their turn.

This system protects families during a vulnerable time while still recognizing legitimate debts. As I often tell clients, “The law tries to balance compassion with responsibility.”

How Liability Is Divided Among Several Transferees

When multiple people receive nonprobate assets, Indiana non probate claims law uses a proportional approach to fairness:

The fair market value test serves as the measuring stick. Each transferee’s liability is based on the percentage of total nonprobate assets they received. For example, if Mom left a $75,000 TOD account to her daughter and a $25,000 POD account to her son (total: $100,000), the daughter would be responsible for 75% of any valid claims against nonprobate assets, while the son would be responsible for 25%.

What happens if one person pays more than their fair share? The law provides reimbursement rights, allowing them to seek contribution from other transferees. This prevents one beneficiary from unfairly shouldering the entire burden.

This proportional approach reflects a fundamental fairness—those who receive more from the deceased’s estate should generally bear more responsibility for the deceased’s debts.

Common Transferee Defenses

Beneficiaries aren’t without protection under Indiana non probate claims law. Several important defenses can shield nonprobate transfers from creditor claims:

The missed deadline bar is perhaps the strongest defense. If a creditor fails to meet any of the statutory deadlines (the 5-month service requirement, 7-month written demand, or 9-month filing deadline), their claim is typically barred forever. This strict timeline encourages prompt resolution of estate matters.

Statutory exclusions provide another layer of protection. Remember those assets specifically excluded by the law? Life insurance proceeds, retirement accounts, and property held as tenancy by the entirety aren’t just excluded from probate—they’re typically protected from creditor claims entirely.

Good faith expenditure can also serve as a defense. If a transferee has already spent the assets in good faith before receiving notice of a claim, they may have a valid defense against liability. Similarly, bona fide purchaser protection shields someone who buys nonprobate property from a transferee without knowledge of potential claims.

These defenses highlight why timing matters so much in estate proceedings. Creditors who delay action may find themselves unable to collect, while beneficiaries who receive proper legal guidance can often steer these waters safely.

For specific questions about how these rules apply to your situation, the experienced attorneys at Fritch Law Office can help you understand your rights and responsibilities under Indiana Code Title 32, Article 17, Chapter 13.

Special Rules for Joint Accounts, TOD Deeds, Vehicles, and Real Estate

When it comes to indiana non probate claims law, not all assets are treated equally. Different types of nonprobate transfers come with their own unique rules and considerations that both creditors and beneficiaries need to understand.

Joint Accounts & POD Designations

Bank accounts that pass outside of probate can create interesting situations for creditors and beneficiaries alike. Indiana’s Multiple-Party Account Act provides the framework for how these accounts work when someone passes away.

For joint accounts, a key question is who actually owned the money. If Mom added you to her checking account just for convenience, but all the funds were really hers, creditors may have a stronger claim to those funds despite your name being on the account.

Ownership percentages truly matter here. Courts will often look at who contributed what to determine the true ownership of the account, not just whose names appear on the paperwork.

Banks also have special rights in these situations. If the deceased owed money to the bank itself, the institution can exercise what’s called “set-off rights” – essentially taking what they’re owed before allowing the remaining funds to pass to joint owners or POD beneficiaries.

“I’ve seen many cases where families were surprised to learn that a joint account they thought was protected was actually subject to creditor claims,” says David Fritch of Fritch Law Office. “Understanding the nuances of indiana non probate claims law can help avoid these unwelcome surprises.”

TOD Deeds & Real Estate

Transfer-on-death deeds have become a popular estate planning tool in Indiana, allowing homeowners to pass real estate directly to beneficiaries without probate. However, they come with specific requirements and limitations.

For a TOD deed to be effective, it must comply with the requirements set forth in IC 32-17-14-11. This includes proper execution and, critically, recording the deed with the county recorder’s office during the owner’s lifetime. While the transfer doesn’t actually happen until death, the groundwork must be laid while the owner is still alive.

One important consideration that many people overlook: existing liens don’t disappear when property transfers via a TOD deed. If there’s a mortgage, judgment lien, or tax lien on the property, those encumbrances generally travel with the property to the new owner.

And while TOD deeds do avoid probate, they don’t necessarily shield the property from creditors. Under indiana non probate claims law, if other assets are insufficient to cover legitimate debts, creditors may still reach property transferred through a TOD deed if they follow the proper procedures and timeframes.

Medicaid estate recovery also presents special considerations for TOD deeds, as the state may have improved rights to recover benefits paid from real estate that passes outside of probate.

Motor Vehicles & Watercraft Titles

Indiana offers convenient methods for transferring vehicles and boats without probate, but these transfers still fall under indiana non probate claims law for creditor purposes.

The Indiana Bureau of Motor Vehicles provides Form 205, the Transfer on Death Beneficiary designation for motor vehicles. This simple form allows you to name someone who will automatically receive your vehicle upon your death. Similarly, the Department of Natural Resources offers comparable provisions for boats and other watercraft.

With Indiana’s increased small estate threshold of $100,000 (raised from the previous $50,000 in 2022), vehicles and watercraft can often transfer using the simplified small estate affidavit process rather than formal probate. This makes the transfer process much easier for families, but doesn’t eliminate potential creditor claims.

When helping clients with estate planning, I always remind them that while these transfers avoid probate, they don’t necessarily avoid creditor claims. Understanding the interplay between nonprobate transfers and potential creditor exposure is essential for both those planning their estates and those who stand to inherit.

Practical Steps for Beneficiaries and Creditors

Whether you’re a beneficiary who has received nonprobate assets or a creditor seeking to make a claim, there are practical steps you should take to protect your interests under Indiana non probate claims law.

Actions Beneficiaries Should Take

If you’ve received assets through a nonprobate transfer in Indiana:

-

Confirm exclusions – Verify whether the assets you received fall into one of the statutory exclusions (like life insurance proceeds or retirement accounts).

-

Keep reserve funds – Consider setting aside a portion of the assets for at least nine months to cover potential creditor claims.

-

Negotiate settlements early – If you’re aware of creditor claims, consider negotiating settlements before formal proceedings begin.

-

Document everything – Maintain records of all assets received, their value, and any communications regarding potential claims.

-

Consult with an experienced attorney – Given the complexity of Indiana non probate claims law, professional guidance is often essential.

Ignoring potential creditor claims won’t make them go away and could potentially increase your liability through additional costs and fees.

Actions Creditors Should Take

If you’re a creditor seeking to make claims against nonprobate assets:

-

Monitor probate notices – Watch for published notices of estate administration to ensure you don’t miss filing deadlines.

-

Timely file and serve – Strictly adhere to the 5-month, 7-month, and 9-month deadlines for filing claims, serving transferees, and making written demands.

-

Use certified mail – Send all notices and demands via certified mail with return receipt to document compliance with statutory requirements.

-

Track the nine-month bar – Calendar the absolute nine-month deadline from the date of death, as this is generally the final cutoff for claims.

-

Consider opening an estate if necessary – If no probate estate has been opened, consider petitioning to open one to preserve your claim rights.

The key for creditors is prompt, documented action. The statutory deadlines under Indiana non probate claims law are strictly enforced, and missing them typically results in permanently barred claims.

Frequently Asked Questions about Indiana Nonprobate Claims

What happens if a creditor misses the nine-month deadline?

Missing the nine-month filing deadline under Indiana non probate claims law is serious business. Once that clock runs out, creditors typically find themselves permanently locked out from making claims—no exceptions, no extensions, no second chances.

This deadline stands firm even in situations where you might expect some flexibility. It doesn’t matter if nobody bothered to open a probate estate. It doesn’t matter if the creditor had no idea the debtor had passed away. And it certainly doesn’t matter if the personal representative “forgot” to send proper notices.

“I’ve seen many creditors caught off guard by how absolute this deadline is,” says David Fritch. “The nine-month bar is one of the strongest protections beneficiaries have under Indiana law.”

There are only a tiny handful of exceptions, mainly for certain government claims and for debts that weren’t yet due when the person died. But these exceptions are rare—the rule is designed to provide certainty and closure for families.

Are life insurance proceeds ever reachable by estate creditors?

Good news for life insurance beneficiaries: Indiana law specifically shields these proceeds from creditors’ grasp. Under Indiana Code 32-17-13-1(c), life insurance payments to named beneficiaries are explicitly excluded from the definition of nonprobate transfers that creditors can pursue.

This protection makes life insurance one of the most effective ways to ensure your loved ones actually receive what you intend to leave them. However, there are a few situations where this shield might crack:

If you name your estate as the beneficiary (rather than specific people), those proceeds become part of your probate estate and fair game for creditors. Similarly, if you transferred the policy in a way that courts consider fraudulent, or if you paid premiums using funds that should have gone to creditors, the protection might fail.

But in the vast majority of cases, Indiana non probate claims law keeps life insurance proceeds safely in the hands of your chosen beneficiaries, regardless of what other debts you might leave behind.

Can Medicaid estate recovery reach a transfer-on-death deed?

Yes, your TOD deed property could potentially be reached by Medicaid recovery efforts. If you received Medicaid benefits during your lifetime, Indiana’s Medicaid estate recovery program allows the state to recover those costs from your estate after you’re gone—and that can include property transferred through a TOD deed.

The Indiana Family and Social Services Administration must follow the same statutory deadlines as other creditors, though recent legislation (SEA 18, 2024) created a special 120-day filing requirement for Medicaid claims. This shorter timeline helps families gain clarity sooner about potential Medicaid recovery issues.

Certain situations provide protection from Medicaid recovery. If you have a surviving spouse or dependent child, recovery is typically delayed or limited. The family home often receives special consideration in these cases.

“Medicaid recovery is where federal regulations and Indiana non probate claims law collide,” notes Fritch. “It creates one of the most complicated areas of estate planning, especially for seniors concerned about long-term care costs.”

The intersection of TOD deeds and Medicaid recovery illustrates why thoughtful estate planning with an experienced attorney is so valuable—what seems like a simple solution (like a TOD deed) can have unexpected consequences if Medicaid benefits are part of your life story.

Conclusion

Navigating Indiana non probate claims law requires careful attention to statutory definitions, strict deadlines, and specific procedural requirements. Whether you’re a beneficiary who has received nonprobate assets or a creditor seeking to make a claim against such assets, understanding these rules is essential to protecting your rights.

At Fritch Law Office PC, we’ve helped countless clients in Jasper and throughout Indiana steer these complex waters. Our experienced team provides personalized guidance custom to your specific situation, whether you’re:

- A beneficiary seeking to protect inherited assets from creditor claims

- A creditor trying to recover from nonprobate transfers

- A personal representative managing both probate and nonprobate assets

The key to success in this area is prompt action and strict compliance with statutory deadlines. The nine-month statute of limitations is particularly critical, as it generally represents the absolute cutoff for most claims against nonprobate transfers.

For personalized guidance on your specific situation involving Indiana non probate claims law, contact our office in Jasper, Indiana. We’re here to help you steer these complex legal waters with confidence and clarity.